Hello, my name is Faizal Khan. I am a banker. One question I often receive is whether the statement on the FinCEN website regarding transactions under $1,000 per day per person exempting from being considered money service providers (MSPs) is correct. Firstly, I want to clarify that I am not a lawyer. This is purely my personal opinion, and I recommend consulting a certified lawyer for professional advice, which may require payment. In my opinion, the statement is quite vague. The United States government has set the threshold at $1,000 per day per person, but it is uncertain how many individuals would actually need to send more than $1,000. For instance, if I needed to send $10,000, I could divide it into $500 increments over twenty days to meet that goal. However, it is important to understand that even in such cases, money transmission is still taking place. To fully comprehend the situation, we must consider the broader context of the Bank Secrecy Act and related regulations, such as anti-money laundering laws, the Patriot Act, and individual state laws concerning money transmission. These laws are intentionally designed to be vague, allowing the government to find clauses that can potentially penalize individuals who violate the rules. The government can argue that even if you stay within the $1,000 limit, if you fail to comply with other requirements such as know your customer (KYC) protocols, reporting obligations, or conducting thorough background checks, they can still take action against you. Therefore, in my perspective, relying solely on the $1,000 per day per person limit to determine if you need a money transmitter license is not advisable. It is essential to consider the accompanying caveats and potential requirements for money transmission. The Bank Secrecy Act and the Patriot Act, among others, could impose additional obligations and liabilities....

Award-winning PDF software

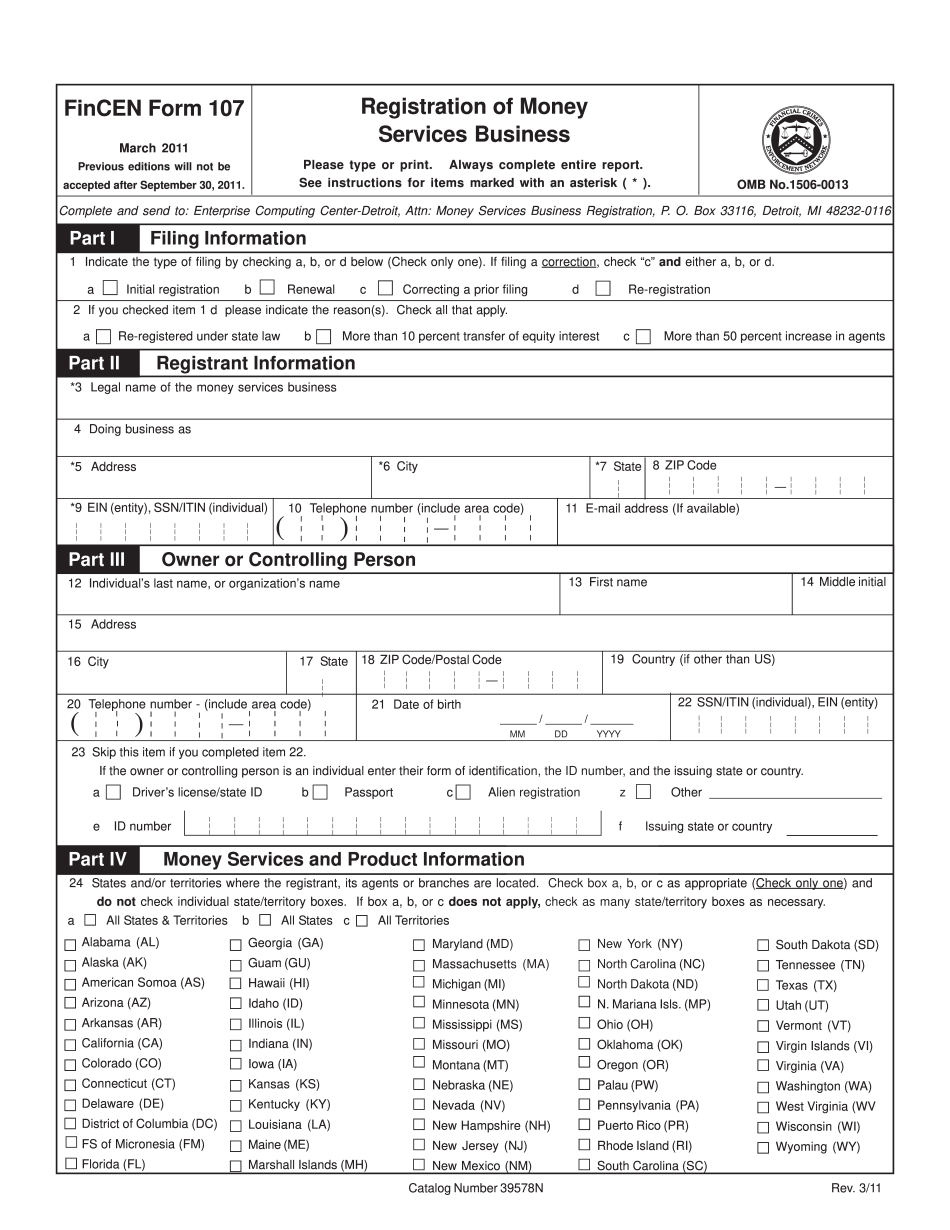

Fincen definition Form: What You Should Know

United States, in which money, assets, funds, or securities are maintained or received, for deposit with or on behalf of the United States or other government or quasi-government agency. Financial institution—(1) All firms, partnerships, insurance companies, investment firms, commercial associations, governmental entities, and persons holding account or receiving deposit, or in any capacity regarding depositors, in any domestic financial institution, whether a national banking association, that has an open accounts with such a national bank; or any other firm, partnership, insurance company, investment firm, commercial association, governmental entity, or person (other than a banking organization or bank) regarding accounts in such an institution. (2) An agent, agency, branch or office within the United States of any person doing business in one or more of the states of Michigan, Indiana, Minnesota or Wisconsin that has a correspondent account or service with such an agent or agency, agency, branch or office, in one or more of the states of Michigan, Indiana, Minnesota or Wisconsin. (3) The term “financial institution” includes, but is not limited to, brokers, dealers, money services businesses, mutual or investment banks, money transmitters, commercial or investment banks, lending banks, savings and loan associations, credit unions, and trust companies; and other financial institutions having the same legal existence but not being licensed by the U.S. Department of the Treasury as a bank. FINANCIAL INSTITUTION AGENCY—Any entity or organization licensed under part 200 of the United States Financial Regulations; any entity or organization whose license or operations is permitted as a banking institution under part 200 of the United States Financial Regulations, or which is exempt from such part. MATERIALS: One or more records. PROCEDURE: See section 3(b) of the BSA E-Filing Instructions for Form 8531 (Reg. S-CFR), and any instructions from a BSA office providing specific instructions (and corresponding information) related to filing a Financial Institution SAR. Routine Operations. Such activities as processing payment or settlement through the institution's systems, if such transactions are made only during a regular business day. SAR Processing Services.

online solutions help you to manage your record administration along with raise the efficiency of the workflows. Stick to the fast guide to do Form Fincen 107, steer clear of blunders along with furnish it in a timely manner:

How to complete any Form Fincen 107 online: - On the site with all the document, click on Begin immediately along with complete for the editor.

- Use your indications to submit established track record areas.

- Add your own info and speak to data.

- Make sure that you enter correct details and numbers throughout suitable areas.

- Very carefully confirm the content of the form as well as grammar along with punctuational.

- Navigate to Support area when you have questions or perhaps handle our assistance team.

- Place an electronic digital unique in your Form Fincen 107 by using Sign Device.

- After the form is fully gone, media Completed.

- Deliver the particular prepared document by way of electronic mail or facsimile, art print it out or perhaps reduce the gadget.

PDF editor permits you to help make changes to your Form Fincen 107 from the internet connected gadget, personalize it based on your requirements, indicator this in electronic format and also disperse differently.

Video instructions and help with filling out and completing Fincen definition